Will The Gig Economy Change Mortgage Lending?

Mortgage Lending and the Gig Economy

Mortgage lenders are facing a new crisis. That is how to deal with loan applications from people who work “by the gig”. And, as more millennials apply for mortgage loans, the entire concept of mortgage lending and the gig economy will become an ever greater issue.

In the past, when it comes to mortgage applications, every loan officer asks the same question. “How long have you been employed at your current job?” they ask. “Two years? Great. Now let’s talk about those pesky debts…”

The implications here are very simple. First, employment equals stability. Second, two years of stability is the minimum threshold lenders would like to see.

These long-term standards are now in flux. When it comes to mortgage lending and the gig economy, it’s become increasingly clear that traditional views of employment aren’t all they’re cracked up to be – especially when it comes time to get a mortgage. For example, rather than two years of iron-clad documentation, Fannie Mae and Freddie Mac now say as little as 12 months of self-employment are enough, as long as the applicant’s previous employment is in the same field and his or her income remains steady.

Going from two years to one year is an important advance. But, the big question is what happens as the concept of work continues to evolve?

First, the old idea of a 40-hour workweek is dead and gone. The average workweek is now less than 35 hours, in part because the Fair Labor Standards Act says covered employees must receive time and a half after 40 hours.

Second, an official place of employment – a formal office setting – may not be part of the job picture

According to the Bureau of Labor Statistics, “In 2016, on days they worked, 22 percent of employed persons did some or all of their work at home.

The bureau says, “Among workers age 25 and over, those with an advanced degree were more likely to work at home than were persons with less education – 43 percent of workers with an advanced degree performed some work at home on days worked, compared with 12 percent of those with a high school diploma.”

“Fortune 1000 companies around the globe are entirely revamping their space around the fact that employees are already mobile,” says GlobalWorkplaceAnalytic.com in a June report. “Studies repeatedly show they are not at their desk 50-60 percent of the time.”

For lenders, the problem with shifting job patterns is that the lines between employment and non-employment have become blurry. Yes, sure, you have a job with Universal Gigantic Industries, a division of Global Pelts, Earwax & Wood chips, but you only visit the company offices once every 14 months – plus you have a few jobs on the side. What’s a mortgage broker to do?

Writing in The New Yorker, Nathan Heller explains, “The American workplace is both a seat of national identity and a site of chronic upheaval and shame. The industry that drove America’s rise in the nineteenth century was often inhumane. The twentieth-century corrective – a corporate workplace of rules, hierarchies, collective bargaining, triplicate forms – brought its own unfairness. Gigging reflects the endlessly personalizable values of our own era, but its social effects, untried by time, remain uncertain.”

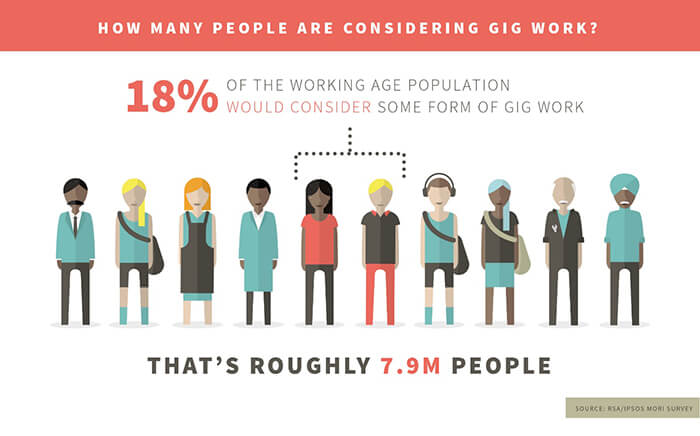

According to the Pew Research Center, “24 percent of Americans report earning money from the digital ‘platform economy’ in the past year.” People like the cash and flexibility, while critics worry that, in too many cases, the “sharing” economy really means little income, on-demand work schedules and no benefits.

Airbnb describes itself as “a new resource for middle-class families” and says “money earned from home-sharing helps nearly 60 percent of Airbnb hosts stay in their homes.”

“For the women and men who drive with Uber,” says the company, “our app represents a flexible new way to earn money. For cities, we help strengthen local economies, improve access to transportation, and make streets safer. When you make transportation as reliable as running water, everyone benefits. Especially when it’s snowing outside.”

For lenders, the gig economy is new and complex and will likely result in an entirely new set of underwriting rules,” says Rick Sharga, executive vice president at Ten-X.com, an online real estate marketplace.

“For example, does income from renting a room count for mortgage qualification purposes if such revenue violates state rules? If someone rents out all or part of his home, does he need residential or commercial financing? Does he own a home or a hotel? What kind of insurance should lenders require?” Sharga comments.

So, what will happen in the future? Today’s hard and fast underwriting rules defining “employment” will have to evolve, just like the rules concerning short-term room rentals and freelance cabbing are changing – otherwise, a large and growing number of mortgages will not be originated, and that’s a result no one will accept.

Mortgage brokers looking to increase their business now can call the professionals at Dataman Group at 800-771-3282 or visit the Mortgage section of the Dataman Group website for more information.

Thank you to Peter G. Miller, a nationally syndicated newspaper columnist, the original creator and host of the AOL Real Estate Center, and the author of numerous books published by Harper & Row for much of the info in this article.