Retirees and Reverse Mortgage Fundedness

When it comes to retirees, the big question is how can reverse mortgage fundedness help retirees? Can a reverse mortgage factor into retirement planning? How does one fund their retirement?

In Tools for Retirement Planning, Tom Davison wrote this about Steven Sass. He is a research economist at the Center for Retirement Research at Boston College. Mr. Sass coined the phrase “Fundedness” as related to preparedness for retirement.

His recent research brief is entitled “Is Home Equity an Underutilized Retirement Asset?”. In this brief, Steven Sass observed that retirement planning generally focuses on the use of financial assets. He also found that “home equity is the largest store of savings for most households entering retirement.” Similarly, for many households, particularly those with less wealth, home equity is larger than their financial assets.

Mr. Sass defined the concept of how adequately funded a homeowner is for retirement. He even gave it a name: “Fundedness”. Fundedness reflects how well a family’s has funded their goals for the future. Most noteworthy, it’s about understanding how their financial resources match those retirement needs and desires.

Diving into Reverse Mortgage Fundedness

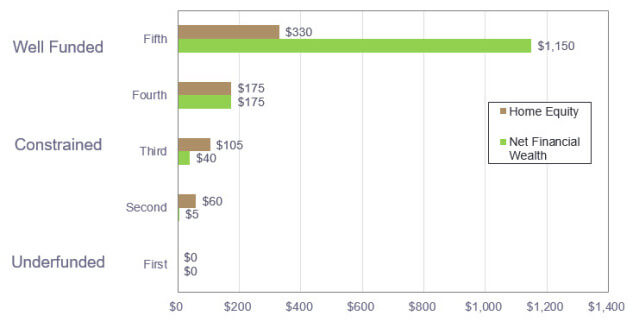

Mr. Sass analyzed home equity and financial wealth across households ages 65-69. This helped him gain a better understanding of Fundedness in 2015 dollars.

He divided the universe into 3 segments. They are Well Funded, Constrained and Underfunded. If you look at the graph below, you can see how Mr. Sass broke out his segments.

No real surprises in the findings.

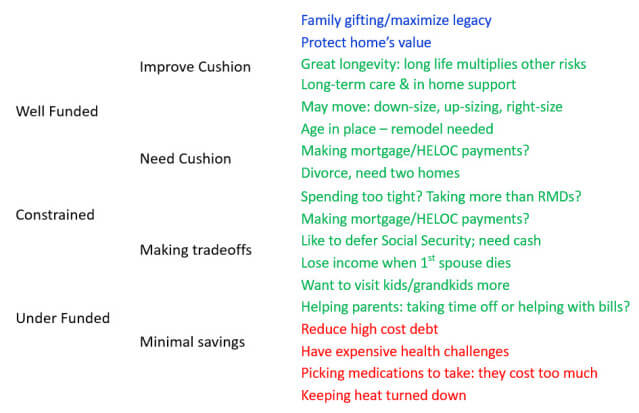

Typically, more affluent people fund their retirement more fully. Many homeowners that haven’t been able to. Sass felt that these Fundedness factors can help us understand the different segments. These Fundedness factors define how homeowners might use the equity in their homes. As a result, they can live a more fulfilling life by using a reverse mortgage.

According to Sass, there is tremendous value in reverse mortgages. Above all, it’s all about what the retirees would be using their reverse mortgages to fund.

The Challenge for Mortgage Marketers

The challenge for mortgage brokers and financial professionals is to find the right reverse mortgage prospects. Using this kind of information, we can target good prospects. With today’s technology, we can select homeowners who could make best use of a reverse mortgage.

Mortgage companies looking to contact reverse mortgage prospects can also get a listing of actual HECM loan holders for refinancing.

To read more from the Dataman Group Direct Mortgage Marketing Blog – click HERE